In some cases it makes good sense to pay more upfronteven buying "points" on your loanif it lets you lock in a low rate for the long term. You can pay mortgage or discounts point charges to the lending institution at closing in exchange for a lesser rates of interest. You'll probably need to pay mortgage insurance if you make a deposit of less than 20%.

Look for a way to come up with 20%. You can't truly eliminate the cost of mortgage insurance coverage unless you re-finance with some loans, such as FHA loans, however you can frequently get the requirement removed when you develop at least 20% in equity. You'll need to pay many costs when you get a home mortgage.

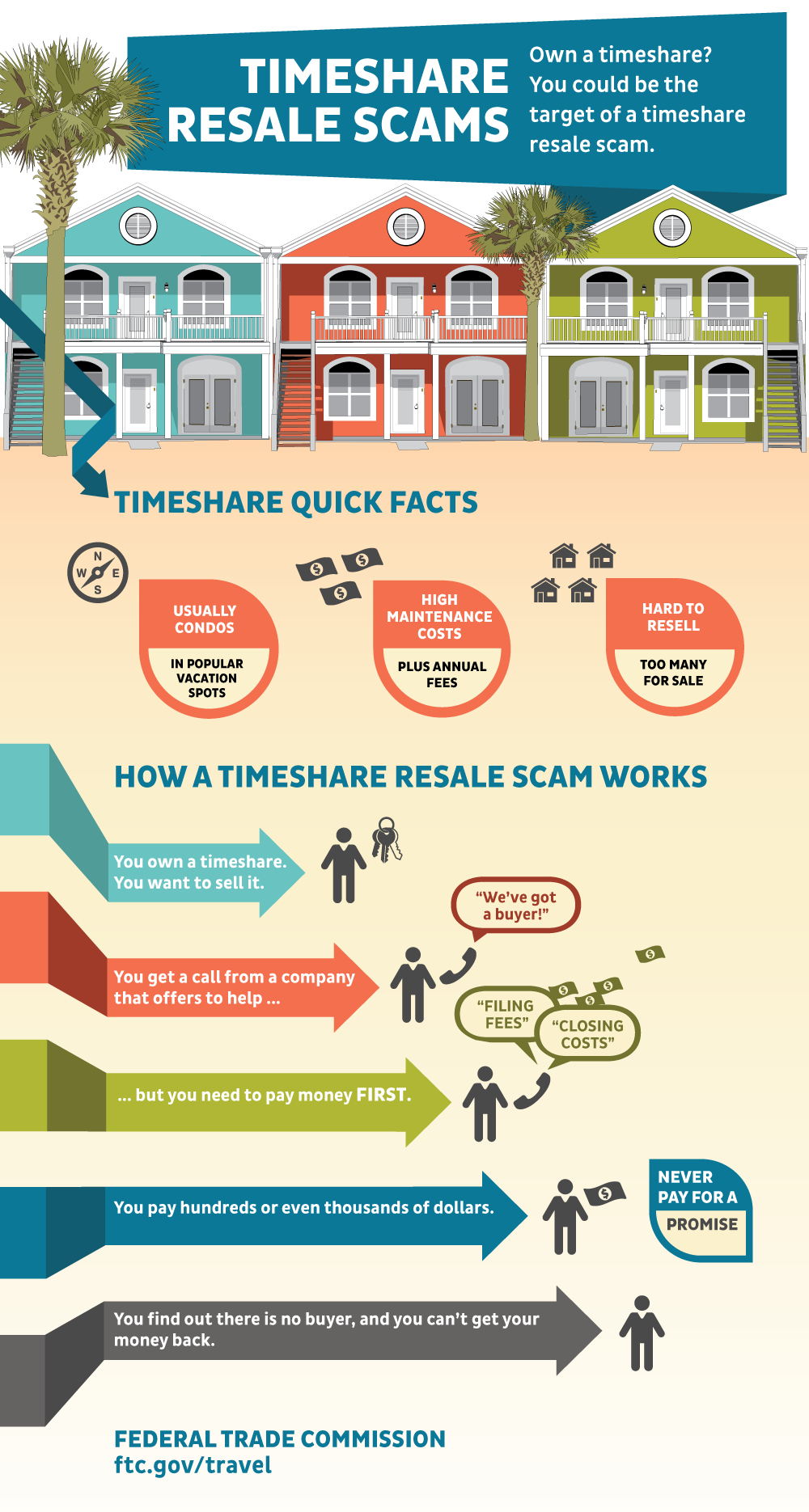

Be wary of "no closing cost" loans unless you make certain you'll only be in the house for a brief time period due to the fact that they can wind up costing you more over the life of the loan.

The American dream is the belief that, through effort, guts, and determination, each person can accomplish financial prosperity. Many people interpret this to suggest a successful career, status seeking, and owning a house, a car, and a household with 2.5 children and a pet. The core of this dream is based on owning a home.

A home loan is simply a long-term loan given by a bank or other financing institution that is secured by a specific piece of realty. If you fail to make timely payments, the lender can repossess the property. Since houses tend to be costly - as are the loans to spend for them - banks permit you to repay them over extended periods of time, referred to as the "term".

Shorter terms might have lower interest rates than their comparable long-term bros. Nevertheless, longer-term loans may use the advantage of having lower regular monthly payments, due to the fact that you're taking more time to pay off the debt. In the old days, a neighboring savings and loan might provide you cash to acquire your home if it had sufficient cash lying around from its deposits.

The bank that holds your loan is accountable mostly for "maintenance" it. When you have a mortgage, your month-to-month payment will generally include the following: A quantity for the primary amount of the balance An amount for interest owed on that balance Real estate taxes Homeowner's insurance coverage Home Home mortgage interest rates come in numerous ranges.

With an "adjustable rate" the interest rate changes based upon a defined index. As a result, your month-to-month payment amount will fluctuate. Home loan can be found in a variety of types, including traditional, non-conventional, set and variable-rate, home equity loans, interest-only and reverse home loans. At Mortgageloan.com, we can assist make this part of your American dream as simple as apple pie.

If you're going to be accountable for paying a mortgage for the next thirty years, you ought to know exactly what a mortgage is. A mortgage has 3 standard parts: a down payment, monthly payments and costs. Since home loans typically involve a long-term payment plan, it's essential to comprehend how they work.

is the amount required to pay off the home mortgage over the length of the loan and consists of a payment on the principal of the loan along with interest. There are typically property taxes and other charges consisted of in the month-to-month expense. are various costs you have to pay up front to get the loan.

The larger your down payment, the better your financing offer will be. You'll get a lower home mortgage rate of interest, pay less charges and gain equity in your house more rapidly. Have a great deal of questions about mortgages? Take a look at the Customer Financial Protection Bureau's answers to often asked questions. There are 2 main types of home loans: a traditional loan, guaranteed by a personal lending institution or banking institution and a government-backed loan.

This eliminates the requirement for a deposit and likewise avoids the requirement for PMI (personal home loan insurance) requirements. There are programs that will assist you in obtaining and funding a home mortgage. Inspect with your bank, city advancement office or a well-informed realty agent to find out more. The majority of government-backed mortgages can be found in one of 3 forms: The U.S.

The primary step to receive a VA loan is to obtain Helpful hints a certificate of eligibility, then submit it with your most current discharge or separation release documents to a VA eligibility center. The FHA was created to assist individuals obtain cost effective housing. FHA loans are actually made by a loan provider, such as a bank, but the federal government guarantees the loan.

Backed by the U.S. Department of Farming, USDA loans are for rural property purchasers who are without "decent, safe and sanitary housing," are not able to protect a home mortgage from traditional sources and have an adjusted earnings at or listed below the low-income limit for the area where they live. After you choose your loan, you'll choose whether you want a repaired or an adjustable rate.

A set rate home loan requires a monthly payment that is the exact same amount throughout the term of the loan. When you sign the loan papers, you settle on an interest rate and that rate never ever changes. This is the best type of loan if interest rates are low when you get a mortgage.

If rates go up, so will your mortgage rate and regular monthly payment. If rates increase a lot, you might be in big trouble. If rates decrease, your home loan rate will drop and so will your monthly payment. It is usually best to stick with a fixed rate loan to safeguard against rising rates of interest.

The amount of cash you obtain impacts your interest rate. House loan sizes fall under two primary size categories: conforming and nonconforming. Conforming loans satisfy the loan limit standards set by government-sponsored home loan associations Fannie Mae and Freddie Mac. Non-conforming loans consist of those made to customers with poor credit, high financial https://www.slideserve.com/inbard9l2r/what-is-the-average-cost-to-get-out-of-a-timeshare-powerpoint-ppt-presentation obligation or recent bankruptcies.

If you desire a home that's priced above your local limit, you can still certify for a conforming loan if you have a huge enough down payment to bring the loan amount down below the limitation. You can reduce the rate of interest on your home loan by paying an up-front fee, called mortgage points, which consequently lower your regular monthly payment.

In this method, purchasing points is stated to be "buying down the rate." Points can likewise be tax-deductible if the purchase is for your primary house. If you prepare on living in your next house for a minimum of a years, then points might be a great option for you. Paying points will cost you more than simply initially paying a greater rate of interest on the loan if you prepare to sell the property within just the next few years.